(Image credit: Shutterstock, Edited by Tom’s Hardware)

A bill proposed in New York state by state Sen. Kevin S. Parker could stop cryptocurrency mining to study and issue findings on how it affects the environment. The bill, NY State Senate Bill S6486, was first reported on by Earther.

Beyond making PC components notoriously difficult to find, running powerful computers day in and day out uses huge amounts of electricity.

The bill, which is still in committee so could change, calls for a “three-year moratorium on the operation of cryptocurrency mining centers in the state, including, but not limited to cryptocurrency mining centers located in converted fossil fuel power plants.” There has been an increase in mining activity in upstate New York. In the town of Dresden, one plant planned “to quadruple the power used to process Bitcoin transactions by late next year,” much to the concerns of environmentalists.

It isn’t completely clear what makes a “cryptocurrency mining center,” and if individuals mining on their own computers would also be banned. Tom’s Hardware has reached out to Sen. Parker’s office and will update this story if we get a response.

Following the environmental impact studies, mining operations that negatively impact greenhouse gas emission targets in the state’s Climate Leadership and Community Protection Act of 2019 would be ineligible to obtain a permit to continue running. That act requires that greenhouse gas emissions across the state be reduced 85% and that it achieves net zero emissions across industries.

The bill cites statistics estimating that cryptocurrency networks use as much energy as Sweden. Some cryptocurrency advocates suggest that it is becoming increasingly common for mining to take place using renewable energy. But while using cheap energy makes for increased profits, that energy still often comes from coal.

Bill S6486 is currently in committee. Its next steps would be to go to the floor calendar, pass both the state’s senate and assembly and, if it gets through all that, be delivered to and signed or vetoed by the governor.

After about a month of preparation, following the initial mainnet launch, cryptocurrency Chia coin (XCH) has officially started trading — which means it’s possibly preparing to suck up all of the best SSDs like Ethereum (see how to mine Ethereum) has been gobbling up the best graphics cards. Early Chia calculators suggested an estimated starting price of $20 per XCH. That was way off, but with the initial fervor and hype subsiding, we’re ready to look at where things stand and where they might stabilize.

To recap, Chia is a novel approach to cryptocurrencies, ditching the Proof of Work hashing used by most coins (i.e., Bitcoin, Ethereum, Litecoin, Dogecoin, and others) and instead opting for a new Proof of Time and Space algorithm. Using storage capacity helps reduce the potential power footprint, obviously at the cost of storage. And let’s be clear: The amount of storage space (aka netspace) already used by the Chia network is astonishing. It passed 1 EiB (Exbibyte, or 2^60 bytes) of storage on April 28, and just a few days later it’s approaching the 2 EiB mark. Where will it stop? That’s the $21 billion dollar question.

All of that space goes to storing plots of Chia, which are basically massive 101.4GiB Bingo cards. Each online plot has an equal chance, based on the total netspace, of ‘winning’ the block solution. This occurs at a rate of approximately 32 blocks per 10 minutes, with 2 XCH as the reward per block. Right now, assuming every Chia plot was stored on a 10TB HDD (which obviously isn’t accurate, but roll with it for a moment), that would require about 200,000 HDDs worth of Chia farms.

Assuming 5W per HDD, since they’re just sitting idle for the most part, that’s potentially 1 MW of power use. That might sound like a lot, and it is — about 8.8 GWh per year — but it pales in comparison to the amount of power going into Bitcoin and Ethereum. Ethereum, as an example, currently uses an estimated 41.3 TWh per year of power because it relies primarily on the best mining GPUs, while Bitcoin uses 109.7 TWh per year. That’s around 4,700 and 12,500 times more power than Chia at present, respectively. Of course, Ethereum and Bitcoin are also far more valuable than Chia at current exchange rates, and Chia has a long way to go to prove itself a viable cryptocoin.

(Image credit: Tom’s Hardware)

Back to the launch, though. Only a few cryptocurrency exchanges have picked up XCH trading so far, and none of them are what we would call major exchanges. Considering how many things have gone wrong in the past (like the Turkish exchange where the founder appears to have walked off with $2 billion in Bitcoins), discretion is definitely the best approach. Initially, according to Coinmarketcap, Gate.io accounted for around 65% of transactions, MXC.com was around 34.5%, and Bibox made up the remaining 0.5%. Since then, MSC and Gate.io swapped places, with MXC now sitting at 64% of all transactions.

By way of reference, Gate.io only accounts for around 0.21% of all Bitcoin transactions, and MXC doesn’t even show up on Coinmarketcap’s list of the top 500 BTC exchange pairs. So, we’re talking about small-time trading right now, on riskier platforms, with a total trading volume of around $27 million in the first day. That might sound like a lot, but it’s only a fraction of Bitcoin’s $60 billion or so in daily trade volume.

Chia started at an initial trading price of nearly $1,600 per XCH, peaked in early trading to peak at around $1,800, and has been on a steady downward slope since then. At present, the price seems to mostly have flattened out (at least temporarily) at around $700. It could certainly end up going a lot lower, however, so we wouldn’t recommend betting the farm on Chia, but even at $100 per XCH a lot of miners/crypto-farmers are likely to jump on the bandwagon.

As with many cryptocoins, Chia is searching for equilibrium right now. 10TB of storage dedicated to Chia plots would be enough for a farm of 100 plots and should in theory account for 0.0005% of the netspace. That would mean about 0.046 XCH per day of potential farming, except you’re flying solo (proper Chia pools don’t exist yet), so it would take on average 43 days to farm a block — and that’s assuming netspace doesn’t continue to increase, which it will. But if you could bring in a steady stream of 0.04 XCH per day, even if we lowball things with a value of $100, that’s $4-$5 per day, from a 10TB HDD that only costs about $250. Scale that up to ten drives and you’d be looking at $45 per day, albeit with returns trending downward over time.

GPU miners have paid a lot more than that for similar returns, and the power and complexity of running lots of GPUs (or ASICs) ends up being far higher than running a Chia farm. In fact, the recommended approach to Chia farming is to get the plots set up using a high-end PC, and then connect all the storage to a Raspberry Pi afterwards for low-power farming. You could run around 50 10TB HDDs for the same amount of power as a single RTX 3080 mining Ethereum.

Seed size not to scale. ☺ (Image credit: Shutterstock)

It’s important to note that it takes a decent amount of time to get a Chia farm up and running. If you have a server with a 64-core EPYC processor, 256GB of RAM, and at least 16TB of fast SSD storage, you could potentially create up to 64 plots at a time, at a rate of around six (give or take) hours per group of plots. That’s enough to create 256 plots per day, filling over 2.5 10TB HDDs with data. For a more typical PC, with an 8-core CPU (e.g, Ryzen 7 5800X or Core i9-11900K), 32GB of RAM, and an enterprise SSD with at least 2.4TB of storage, doing eight concurrent plots should be feasible. The higher clocks on consumer CPUs probably mean you could do a group of plots in four hours, which means 48 plots per day occupying about half of a 10TB HDD. That’s still a relatively fast ramp to a bunch of drives running a Chia farm, though.

In either case, the potential returns even with a price of $100 per XCH amount to hundreds of dollars per month. Obviously, that’s way too high of a return rate, so things will continue to change. Keep in mind that where a GPU can cost $15-$20 in power per month (depending on the price of electricity), a hard drive running 24/7 will only cost $0.35. So what’s a reasonable rate of return for filling up a hard drive or SSD and letting it sit, farming Chia? If we target $20 per month for a $250 10TB HDD, then either Chia’s netspace needs to balloon to around 60EiB, or the price needs to drop to around $16 per XCH — or more likely some combination of more netspace and lower prices.

In the meantime, don’t be surprised if prices on storage shoots up. It was already starting to happen, but like the GPU and other component shortages, it might be set to get a lot worse.

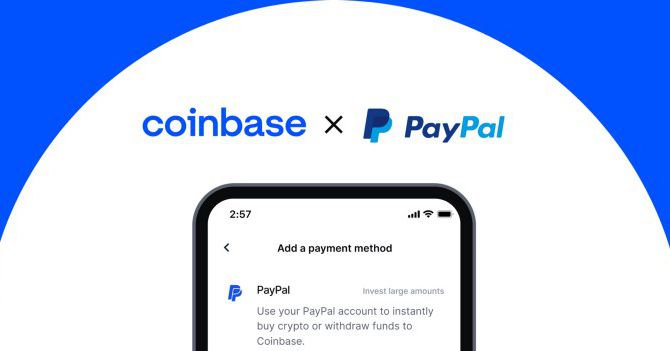

Coinbase has added the option for users to buy cryptocurrency using their PayPal accounts in the US, the company has announced. It says the feature offers a “familiar and trusted” experience for users buying any of the numerous cryptocurrencies that the exchange currently supports, and using PayPal as an intermediary means you don’t have to give your bank account or debit card information directly to the cryptocurrency exchange. The feature will expand to other countries in the coming months.

To use the new option, Coinbase says you can add your PayPal account via the “Add a payment method” option, which links to the PayPal login screen. Purchases made via PayPal are capped at $25,000 a day, or 0.46 Bitcoin as of this writing. Debit cards and bank accounts linked to a PayPal account can be used to buy cryptocurrencies, but a Coinbase FAQ notes the feature doesn’t support payment methods like prepaid cards or credit cards.

A PayPal account can be added from the “Add a payment method” screen.Image: Coinbase

The news is part of PayPal’s broader trend towards embracing cryptocurrency. In November last year, the company started letting US users buy, sell, and hold cryptocurrencies directly from their PayPal accounts, and this year it rolled out the option for users to pay with cryptocurrency held in their PayPal account (though this is converted to local currency before a merchant is paid). PayPal currently only supports four cryptocurrencies natively — Bitcoin, Ethereum, Litecoin, and Bitcoin Cash — compared to the dozens available on Coinbase.

The Department of Justice said it has arrested a Russian-Swedish national who allegedly operated a long-running cryptocurrency laundering site. According to a news release from the DOJ, Roman Sterlingov ran Bitcoin Fog, a cryptocurrency tumbler or “mixer”— which hides a cryptocurrency’s source by mixing it with other funds.

Bitcoin Fog gained “notoriety as a go-to money laundering service for criminals seeking to hide their illicit proceeds from law enforcement,” according to the DOJ. The department says over the course of 10 years, Bitcoin Fog moved more than 1.2 million bitcoin, valued at the time of the transactions at around $335 million.

Bitcoin Fog has received a fair amount of coverage from cryptocurrency blogs and news sites since its inception, with some recommending it as the best option for hiding the origin of bitcoin. The blockchain keeps track of bitcoin transactions, making services like Bitcoin Fog key for those looking to do business on the black market.

“The bulk of this cryptocurrency came from darknet marketplaces and was tied to illegal narcotics, computer fraud and abuse activities, and identity theft,” the DOJ said.

According to the IRS, the largest senders of bitcoin through Bitcoin Fog were “darknet markets, such as Agora, Silk Road 2.0, Silk Road, Evolution, and AlphaBay, that primarily trafficked in illegal narcotics and other illegal goods.”

The IRS said it appeared from Bitcoin Fog transaction activity that Sterlingov took commissions of as much as $8 million on the bitcoin he helped clients launder. The current value of the Bitcoin Fog cluster — the large database of transactions — is about $70 million, the IRS said.

Sterlingov is charged with money laundering, operating an unlicensed money transmitting business, and money transmission without a license in the District of Columbia.

Just when we thought that smart cities, smart factories, IoT devices, autonomous vehicles, and robots will be the main generators of data that will require storage space in the coming years, Chia cryptocurrency just demonstrated that it will also be a formidable generator of data, at least for the time being.

In a about a month’s time storage space allocated to Chia network increased from 120PB all the way to 1143PB, or 1.14 Exabytes. 1.14EB equals 1,140,000TB, or 63,333 20TB hard drives.

(Image credit: Chia)

Chia is a proof of space-time cryptocurrency that uses storage space on farmers’ systems to store a collection of cryptographic numbers called ‘plots.’ When the blockchain broadcasts a challenge for the next block, farmers’ systems scan their plots to see if they have the hash that is closest to the challenge. This method eliminates the Proof of Work concept used by Bitcoin and Ethereum therefore lowering vast power requirements for mining, which developers of Chia call ‘farming.’

Meanwhile, the probability of winning a block is the percentage of the total space that a farmer has compared to the entire network, which essentially means that someone with more available space has more chances to win. So, while accelerators and GPUs are not needed for Chia farming, someone with more storage space to host more plots earns more.

At present each plot requires around 350GB of storage space and 4GB of RAM, so when one wants to store 100 plots, they need a system with 35TB of space and 400GB of RAM. While buying four 10TB HDDs is not cheap, 400GB of RAM (and host CPUs to support them) cost a lot.

(Image credit: https://github.com/xorinox)

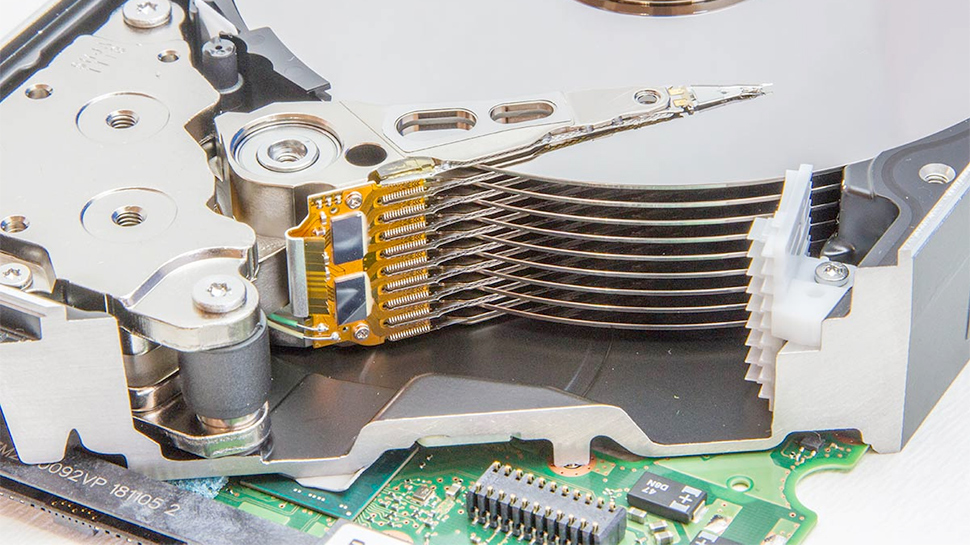

Thousands of Chia farmers now build machines with tens of HDDs that can store tens terabytes of data. While one of such drives does not consume a lot — about 6.5W when operating and about 5.6W when idling — tens of such HDDs can consume hundreds of Watts when they work and usually more when starting up. For example, a system with 32 Western Digital HC550 18TB HDDs (like the one pictured above) powered by a monster motherboard with 32 SATA ports can consume around 180W when idling, which does not count power consumption of memory and compute modules.

For obvious reasons, there are no consumer PC chassis or NAS boxes with 32 3.5-inch bays. Meanwhile, rack-based chassis with backplanes for data centers are quite expensive. As a result, hardware used for Chia farming is either DIY or designed specifically for this purpose and nothing else. Essentially, in just about several months’ time a new segment of hardware market for Chia farming has developed.

It remains to be seen how Chia cryptocurrency mining will develop going forward. But at this rate the amount of storage space used by Chia network will be gargantuan a year from now.

Bitcoin mining fever has some severe symptoms. While some think it’s a good idea to mod a Gameboy to mine Bitcoin, others prefer the more retro Commodore 64 for that purpose. It certainly won’t rival any ASIC miner out there, but it still is an achievement worthy of being shared.

Who thought that when the Commodore 64 was launched in 1982, that it would eventually be used for crypto mining? For those who don’t know, the Commodore 64 is an 8-bit home computer developed by CBM featuring a MOS Technology 6510 processor clocked at 0.985-1,023MHz (depending on the version). The console had 64KB of RAM and 20KB of ROM was launched with an MSRP of $595.

Back then, the specifications were quite beefy, but aren’t exactly up to modern standards. Still, that doesn’t make the machine any less capable of cryptomining, as we see in 8-Bit Show and Tell’s video. Using YTM/Elysium’s Bitcoin Miner 64 and a few other adaptations, the Commodore 64 can successfully mine Bitcoin.

Mining performance was really bad, with a hash rate of 0.3H/s, but it could easily be 10x higher if the miner was built on Commodore 64’s language. The modder even used the SuperCPU 20MHz 65816 processor upgrade, which improved the C64’s mining performance by about 20x.

Discuss on our Facebook page, HERE.

KitGuru says: The viability of using a retro console to mine Bitcoin is quite low, but those who can pull such things deserve some merit. Do you have a Commodore 64 lying around in your house somewhere?

Become a Patron!

Check Also

Samsung admits that TV production could be affected by the ongoing chip shortage

The chip shortage is really causing quite the stir in the electronics industry. Besides GPUs …

Bitcoin is falling back to earth. This morning, the cryptocurrency’s price was nearly 25% lower than the all-time high set a few weeks ago, and reports that U.S. President Joe Biden plans to nearly double the capital gains tax might be partly responsible.

The cryptocurrency’s value peaked at nearly $65,000 per coin on April 13 as the Coinbase trading platform prepared to go public. Its per-coin price fell as low as $47,467 this morning, according to Coindesk, before starting to rebound.

It’s possible that Bitcoin’s value would have fallen even without the Bloomberg report Thursday afternoon on President Biden’s planned increase to the capital gains tax. The crypto market is fickle, and not even Bitcoin’s price can be expected to rise forever.

Other cryptocurrencies have also declined in value today. Coindesk’s data puts Ethereum’s price down 10.5% in the last 24 hours, and it’s fared better than other coins, some of which have seen their prices fall by as much as 24% at time of writing.

Even the beloved Dogecoin, returns for which rose 6,000% year-over-year just last week, has seen its per-coin price fall by roughly 20%. But at least Dogecoin is a meme rather than the cornerstone of an entire industry.

Does this mean the crypto boom is over? Probably not. The market isn’t known for its stability, and efforts to capitalize on it will continue, despite these falling prices. And, of course, we doubt it’ll be easier to find the best graphics cards today than it was yesterday.

But at least enthusiasts who missed out on the Bitcoin craze will be able to watch the cryptocurrency’s price fall for a while instead of climbing up, up, up like it was before.

Researchers have discovered that the XCSSET malware has started targeting M1-equipped Macs via Xcode, The Hacker News reported Monday and has been updated to compromise accounts on various cryptocurrency trading platforms.

Xcode is the integrated development environment (IDE) used to make apps for the iPhone, iPad, and other Apple hardware. Even if a cross-platform framework is used to develop a particular app, it must pass through Xcode to reach those platforms.

That means XCCSET is limiting itself to technically savvy people who, if we had to guess, would be more likely to own cryptocurrency than the average Mac owner. Targeted attacks like this are often more successful than broader ones.

Kaspersky warned that XCSSET had been updated for Apple’s custom silicon in March. The malware wasn’t focused on cryptocurrency at the time, the security company said. Instead, it featured a variety of modules that were designed to:

Reading and dumping Safari cookies

Injecting malicious JavaScript code into various websites

Stealing user files and information from applications, such as Notes, WeChat, Skype, Telegram, etc.

Encrypting user files

Trend Micro then warned on April 16 that XCSSET had been updated to bypass security features introduced with macOS Big Sur, change the icons it uses to match system icons, and attempt to gain access to victims’ accounts on crypto platforms.

The company’s advice was clear: “To protect systems from this type of threat, users should only download apps from official and legitimate marketplaces,” it said. But that’s hard to do when it comes to finding Xcode projects to work with or learn from.

XCSSET’s expansion to cryptocurrency makes sense. The value of Bitcoin, Ethereum, and even Dogecoin has continued to rise in recent months, and stealing coins from someone else is probably requires fewer resources than mining them would.

Adding support for Apple’s custom silicon was also prudent. Devices featuring the M1 chip have been well-reviewed, and with Apple’s plan to ditch Intel entirely by the end of 2022, it makes sense to start targeting its chips now.

Other malware creators appear to agree. We saw reports of the first malware targeting Apple silicon in February, and in March, the Silver Sparrow malware was discovered on approximately 30,000 macOS devices, some of which had M1 chips.

If you have tons of Dogecoins lying around, you can use them to put together your next PC or upgrade. Newegg has announced via a press release today that the retailer now accepts Dogecoin as a payment method.

Newegg has always been a retailer that embraces cryptocurrencies. The company was one of the first to accept Bitcoin back in 2014 and now, the online retailer has added Dogecoin to the list. Using Dogecoin on Newegg is as easy as selecting your BitPay wallet at checkout and then choosing the Dogecoin option.

“The excitement and momentum around cryptocurrency are undeniable, and the recent surge in Dogecoin value underscores the need to make it easier for customers to make purchases with this popular cryptocurrency,” said Andrew Choi, Sr. Brand Manager of Newegg. “We’re committed to making it easy for our customers to shop however works best for them, and that means letting them complete transactions with the payment method that suits them best. To that end, we’re happy to give Dogecoin fans an easy way to shop online for tech.”

In comparison to Bitcoin, Dogecoin is easier to mine. However, the reward is also lower. While a Bitcoin is worth over $56,000, Dogecoin is currently sitting at $0.39. Just a week ago, the meme-inspired cryptocurrency was worth $0.09 so that’s a whopping 355% increase. According to data from CoinMarketCap, Dogecoin’s current market cap is over $50 billion, which is even bigger than Ford Motor Co. and just a few million behind Twitter.

You can pick up some good stuff if you’ve been stashing Dogecoins. The GeForce RTX 3090, when in stock, starts at $1,499 at Newegg, which is equivalent to around 4,470 Dogecoins with today’s rate. Or if you’re into consoles, the PlayStation 5 sells for just $2,099.99 or 6,255 Dogecoins.

Venmo is releasing a feature that will allow users the option to store, buy, and sell popular cryptocurrencies, PayPal announced on Tuesday. Similar to PayPal, Venmo will support four different cryptocurrencies: Bitcoin, Ethereum, Bitcoin Cash, and Litecoin. PayPal had said last year that Venmo would get support for cryptocurrencies.

You can get started with as little as $1, and transactions are managed from the app. Venmo said in a press release that it will begin rolling out the feature to some users today, and tells The Verge it anticipates that “most customers” will have access to cryptocurrencies in the app by the end of May.

All cryptocurrency transactions will be managed directly from the Venmo app.Image: Venmo

Venmo’s support for cryptocurrencies could encourage more people to invest in them. PayPal reported in 2019 that Venmo had 40 million users; given the app operates like a social network, users may find cryptocurrency more approachable if they can see their friends buying and selling right inside Venmo.

Venmo is the latest payment app to offer support for cryptocurrency. PayPal allowed users to buy, hold, and sell cryptocurrency from the main PayPal app in November and added the ability for US users to make purchases with cryptocurrency in late March. And Venmo and PayPal competitor Square launched support for Bitcoin in its Cash App in 2018.

With the emergence of the Chia cryptocurrency, miners in China are reportedly frantically snatching up every hard drive and SSD they can find. Unlike other cryptocurrencies, you don’t mine Chia with a processor, graphics card or ASIC miner. Instead, you farm Chia with storage space, which is where hard drives or SSDs come in. Chia isn’t officially available for trading yet, therefore, it’s too early to start hoarding hard drives or SSDs.

Unlike Bitcoin, which is based on proof of work, Chia utilizes a proof of space and time model. Chia reportedly arrives as an eco-friendly cryptocurrency. Bram Cohen, who’s best known as the inventor of BitTorrent, created Chia to leverage the free space on storage devices. The basis behind Chia is that hard drives and SSDs use less power, are easier to come by and cheaper to purchase. By comparison, mining Ethereum or Bitcoin on a mass scale contributes to the electricity waste.

According to HKEPC’s report, miners are mass purchasing hard drives that span from 4TB to 18TB in capacity. The panic buying will ultimately lead to a hard drive shortage and price hikes. In Hong Kong, hard drive and SSD pricing is expected to increase between 200 HKD to $600 HKD (~$26 to $77). Due to the constant read and write operations, consumer SSDs aren’t the first choice for farming Chia. Nothing is safe from miners though when a profit is there to be made though.

Jiahe Jinwei, one of the big domestic manufacturers in China, told media outlet MyDrivers that the company’s Gloway and Asgard high-performance 1TB and 2TB NVMe M.2 SSDs are all sold out. The manufacturer plans to put restrictions in place to stop miners from buying enormous amounts of consumer SSDs. Subsequently, the company will also increase production to meet the demand. Apparently, Jiahe Jinwei is even developing a specialized SSD for mining operations.

Farming on a consumer SSD is viable, but the more serious miners will likely look to the enterprise side. Endurance is just as important as capacity and performance, and enterprise or data center SSDs typically meet these three criteria.

Many cryptocurrencies come and go so it’ll be interesting to see how Chia pans out. A few years ago, no one took Bitcoin seriously, and today it’s worth over $62,000.

There’s no denying that Dogecoin is a meme. It’s also proven to be quite valuable to those who decided to buy in, with Coindesk today reporting that returns on the coin have risen 6,000% this year — and over 450% just in the past week — despite the fact that it was specifically created as a joke.

Dogecoin was created in 2013 as “an open source peer-to-peer digital currency, favored by Shiba Inus worldwide,” as its official website proclaims. It also offers a helpful conversion tool that explains 1 Dogecoin = 1 Dogecoin. Mind, blown.

But if there are three safe-for-work things people love on the internet, they’re dogs, memes and cryptocurrencies. Redditors are particularly fond of Dogecoin, and they often gift the financially viable meme to people whose posts they’ve enjoyed.

All of which makes Dogecoin a low-priced cryptocurrency (more on that in a moment) that’s also popular on one of the world’s most-visited social platforms. No wonder CoinGecko puts it as the fifth most-traded coin on popular exchanges.

Let’s be clear: Nobody’s getting rich by owning a few Dogecoin. Coindesk’s data puts the coin’s price at $0.005405 on January 1; it peaked at $0.434727 this morning. That means $1 is worth the same as roughly 2.3 Dogecoins at its highest price to date.

Even pennies add up over time, however, and at time of writing CoinGecko puts Dogecoin’s market cap at nearly $45 billion. Newsweek also reported today that Dogecoin made a man from Los Angeles a millionaire.

So is Dogecoin even close to Bitcoin in terms of market cap or value? No. Bitcoin’s market cap is over $1 trillion, and it’s currently priced at around $61,500 per coin, according to CoinMarketCap. No other cryptocurrency even comes close on either metric.

But there’s another key difference: Dogecoin is a meme; Bitcoin is supposed to be the future of the global economy. (At least according to those who stand most to profit from it becoming as such.) The fact that anyone’s even talking about Dogecoin eight years after its introduction is both a miracle and a bit of a meme unto itself.

Dogecoin’s ascendance could also have a similar—but obviously much smaller—effect on the cryptocurrency market as Bitcoin’s. Rapid increases to one coin’s value often result in, or are at least accompanied by, price bumps for other coins as well.

That could hold especially true for other “Memecoins” that were created more as performance art than actual currency. Or maybe Dogecoin is the only one that will ever be worth anything. We’re talking about the economics of an eight-year-old meme coin with a dog’s face on it; does any of this seem predictable?

Oh, super, Dogecoin is spiking. The joke currency, which as recently as January 27th was worth less than a cent, hit 47 cents this morning, according to Robinhood’s tracker. As I type this, the market cap is more than $51 billion.

The currency is based on an au-courant-as-of-2013 meme of a Shiba Inu, and was intended to satirize bitcoin. Well, kids, the joke’s over. It’s now a top-10 cryptocurrency.

Weird year for finance, honestly. There was the Gamestonk thing which made GameStop stock so valuable, a member of the board of directors had to step down so that he could sell shares without restrictions. (Noted investor David Einhorn accused Elon Musk of pouring “jet fuel” on the January rally; a hedge fund called the top of the January rally based on the Musk tweet and raked in the dough.) Keith “Roaring Kitty” Gill stands to make millions, which he will presumably use to buy fancier headbands. NFT mania seized the world, after artist Beeple — aka Mike Winkelmann — sold an NFT of Everydays: The First 5,000 Days for $69 million. Coinbase went public earlier this week, and closed its first day of trading worth more than the company behind the Nasdaq, the exchange it trades on.

Last night, Musk — a shitposter with a hobby of being CEO of Tesla and SpaceX — tweeted “Doge Barking at the Moon.” For those of you fortunate enough to have avoided internet-related brainworms: a bunch of people probably thought this was a reference to a phrase used by internet traders, “to the moon.” Musk, who is known for coming to memes late, has called dogecoin his favorite cryptocurrency. In February, he called it “The People’s Crypto.”

Look, it’s not my fault that the interest rate is zero percent — that was always gonna make shit weird, because there’s almost nowhere safe to park your money without losing some of it to inflation. That means a lot more money is sloshing around than usual, which is fueling everything from SPACs to Gamestonk. What worries me is that we could be locked into zero interest rate policy world for as long as five years, which is an awfully long time for memes to mess with actual money. As long as there’s this much money sloshing around, anything goes. Anyway, if you are a hedge fund that called the top on Dogecoin based on an Elon Musk tweet, let me know — I’d love to interview you and find out how that call went.

Bitcoin mining is an incredibly resource-intensive process. So what better place to do it than an abandoned power plant? Well, as New York Focus reported this week, Finger Lakes environmentalists think the answer is “pretty much anywhere else.”

The conflict revolves around a power plant on New York’s Seneca Lake called Greenidge. The company’s website says the plant was opened in 1937, shuttered in 2009 and purchased by new owners in 2014. Those owners started mining Bitcoin in 2019.

New York Focus reported that Greenidge plans “to quadruple the power used to process Bitcoin transactions by late next year” as the cryptocurrency’s value soars. Environmentalists fear those plans would lead to dangerously high CO2 emissions.

This isn’t a new concern. Researchers have warned about the environmental implications of cryptocurrency mining for years, claimed that Bitcoin uses more electricity than all of Argentina each year and said the increasing popularity of Bitcoin mining could prevent countries like China from meeting their climate goals.

Yet, those warnings have often been ignored as Bitcoin’s value has risen. That’s unlikely to stop now that the cryptocurrency has a $1 trillion market cap and recently saw its price rise to an all-time high as the Coinbase trading platform went public.

Bitcoin’s defenders often claim that it’s hard to measure the cryptocurrency’s effect on global warming because every mining operation is different. Some could use the cleanest energy sources available; others might be as pollutant as they get.

This is where local conflicts like this come in. New York Focus pointed to the same numbers environmental advocates are using to argue against the company’s plans for expansion.

”Last year, Greenidge’s GHG emissions were far below the plant’s annual allowance of 641,000 tons of CO2-equivalent gasses,“ the report said. “But as Greenidge ramped up Bitcoin transaction processing throughout 2020, its rolling 12-month GHG emissions average soared nearly tenfold, from 28,000 tons in January to 243,000 tons in December.”

Now imagine how things could worsen if Greenidge quadruples power usage as planned. There wouldn’t necessarily be a one-to-one increase, of course, but it’s not hard to figure out why local residents might oppose Greenidge’s expansion plans.

The other fear is that more power plants—which, by their very nature, have access to the massive amounts of electricity required to mine Bitcoin—might follow Greenidge in expanding into the cryptocurrency market.

It’s worth reading the full New York Focus report on Greenidge’s situation, especially if you live in upstate New York, but this should serve as a welcome reminder that Bitcoin’s rise has far greater implications beyond making crypto enthusiasts rich.

According to Reuters the price of Bitcoin reached an all-time high today as Coinbase, a platform for buying and selling cryptocurrency, prepared for its initial public offering. The company is set to be listed on the Nasdaq stock exchange today under the “COIN” ticker symbol.

Coinbase said in the IPO announcement that it‘s “building the cryptoeconomy—a more fair, accessible, efficient, and transparent financial system enabled by crypto.” Time will tell if it will ever realize that goal. As for the company’s effect on Bitcoin’s value, well, that became obvious in the hours leading up to its listing on Nasdaq.

Bitcoin’s price reached $63,191 today, according to Coindesk, which said that is the cryptocurrency’s all-time highest value. It previously peaked at $60,743 per coin in March before the price started to fluctuate between around $55,000 and $59,000.

Those prices make Bitcoin the most significant cryptocurrency by far in terms of market cap. The crypto market writ large had a market cap of $2 trillion earlier this month; Bitcoin represented over $1 trillion of that figure by itself. This new $63,191 peak is well above the $42,000 per coin price needed to maintain that milestone.

Leading the crypto market also means that what’s good for Bitcoin can be good for other cryptocurrencies. Coindesk’s figures indicate that Ethereum’s price has risen fairly steadily throughout the week to a current per-coin value of $2,220 despite a drop earlier in the month. Those increases could be related to Bitcoin’s rise.

That isn’t necessarily good news for enthusiasts looking for the best graphics cards, because Ethereum miners are making it even harder to find recent GPUs in stock amid the global chip shortage, but early cryptocurrency adopters might be able to cash in on Coinbase’s efforts to normalize crypto in the mainstream market.

The silver lining: Bitcoin mining is far more resource-intensive than Ethereum mining. An industrial miner recently purchased $30 million worth of Nvidia’s Cryptocurrency Mining Processor (CMP) offerings. Anyone serious about mining Bitcoin isn’t going to be competing with enthusiasts over a single graphics card.

We use cookies on our website to give you the most relevant experience. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.